Most Americans don’t think about their credit scores enough. Having a good credit score is important when you apply for an auto, student, or home loan; apply to rent an apartment; or apply for a cash-handling job. By the time you realize you need a boost, you might not have enough time to fix your credit score, which might result in a higher interest rate on a loan or credit card account or being declined for an apartment or job.

Lenders rely on credit scores — which range from 300 to 850 — to gauge an applicant’s risk profile. Accordingly, they want to see FICO credit scores as high as possible. NerdWallet data from 2019 shows that the average consumer’s FICO credit score hovers around 704, which is at the lower end of “good” territory but still higher than it had been in the past.

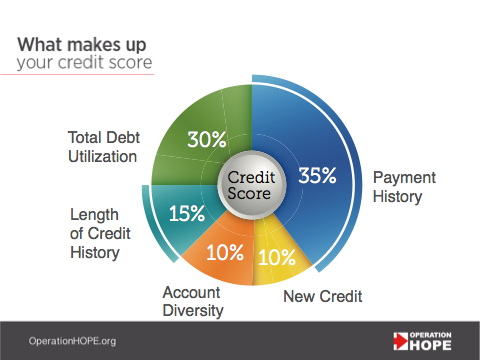

The first step toward boosting a credit score is understanding what makes up your credit score in the first place.

Credit scores are determined based on several key factors, yet not all factors contribute equally to the final number.

Payment history makes up 35% of your credit score. This means that paying bills on time or before their due dates can have the biggest impact on moving the needle.

Total debt utilization — the outstanding balances on revolving accounts such as credit cards or personal lines of credit — makes up 30% of your credit score. Ideally, total debt utilization should be 30% or less of the credit limit. As an example, people with a $1,000 credit card limit should keep a balance of no more than $300 as they try to improve their credit score.

The last three elements that make up your credit score are length of credit history (15%), account diversity (10%), and new credit (10%). Lenders like to see an older credit account because it shows an established record of healthy credit use. And they also want a mix of credit types to show versatility in managing multiple accounts concurrently. As for new credit, every time a credit inquiry is made, it is recorded. Occasional new credit inquiries probably will not affect a credit score too much, but multiple inquiries can cause a negative impact.

Taking all these consumer credit behaviors and backgrounds into consideration, each credit bureau will generate a FICO score on you based on your credit history. Consumers who receive low credit scores should take the rating seriously because a credit score is important. A negative credit rating can result in everything from declined loans and higher interest rates to not being eligible for certain types of employment.

Worried because your credit score is not where you want it to be? There are several ways to gradually and predictably improve and protect your credit score:

You are legally entitled to a free credit report every year from each of the credit bureaus: Equifax, Experian, and TransUnion. You can obtain one online by visiting AnnualCreditReport.com. Examine the report to ensure all information is correct, including account numbers, credit limits, and balances. If you find a discrepancy, you can dispute it with the credit bureau. In fact, a dispute could fix credit score inaccuracies fast. Disputing will not negatively affect your credit score.

A primary cause of a poor credit score is not making payments or only partially paying debt without negotiating a new payment arrangement with creditors first. If you consistently run out of money before your bills are paid, create a household budget to track your spending. You might also want to schedule your bills on your calendar app in advance of their due dates. Your goal is to chip away at payments in arrears. After seven years, missed and late payment history will drop from your credit score.

Have you maxed out your credit cards? You are only hurting your credit and taking longer to fix your credit score so you can enjoy more financial freedom. Begin to pay down your revolving credit card debt consistently. As you dip below 30% of the limit, your credit score should rise. Lenders like to see a low ratio of use when it comes to available credit. In the future, think twice before using credit cards unless you pay off all or most of the balance monthly.

You might be tempted to close all of your credit accounts, but try to keep the oldest open. You will establish the length of your credit history, which improves your credibility with lenders. You might even want to become an authorized user on someone else’s older credit card account to get a bit of a credit score rise. Just make sure the other person has good credit before you agree to be an authorized user.

Achieving an excellent credit rating takes time. But fixing negative credit scores is not hard. Be patient and stay the course. With proper money management, you can change the way lenders see you.

Operation HOPE is an independent third party unrelated to Cathay Bank and Cathay General Bancorp.

This article does not constitute legal, accounting or other professional advice. Although the information contained herein is intended to be accurate, Cathay Bank does not assume liability for loss or damage due to reliance on such information.